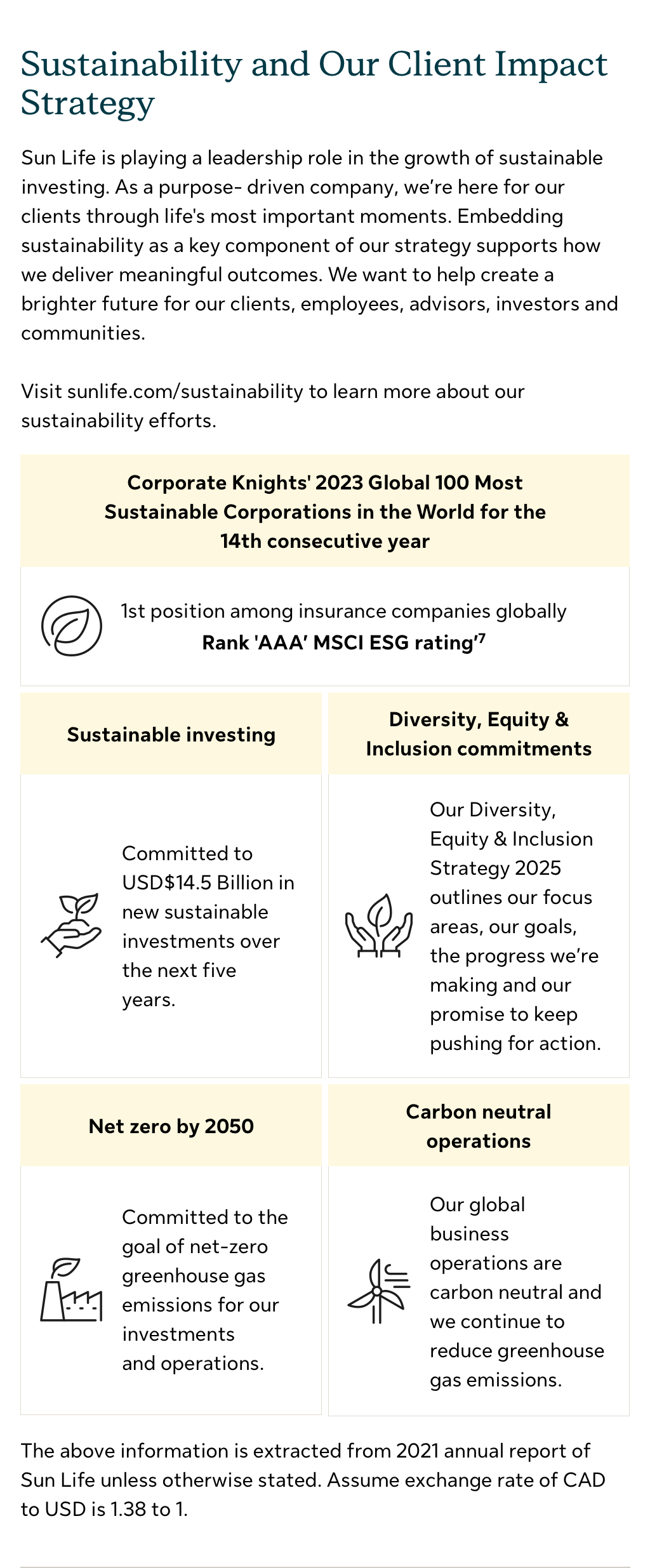

Sun Life HK launched below ESG-focused savings plans to the market that actively integrates ESG concepts into its own investment strategies, managing the risks and optimizing opportunities through focusing investment on those assets with high ESG ratings.

Fulfillment ratios and Total Cash Value ratios of respective products

| Stellar Multi-Currency Plan | SunGift | SunJoy | Stellar |

|---|---|---|---|

| SunProtect | SunGuardian | SunGuardian (Care Version) |

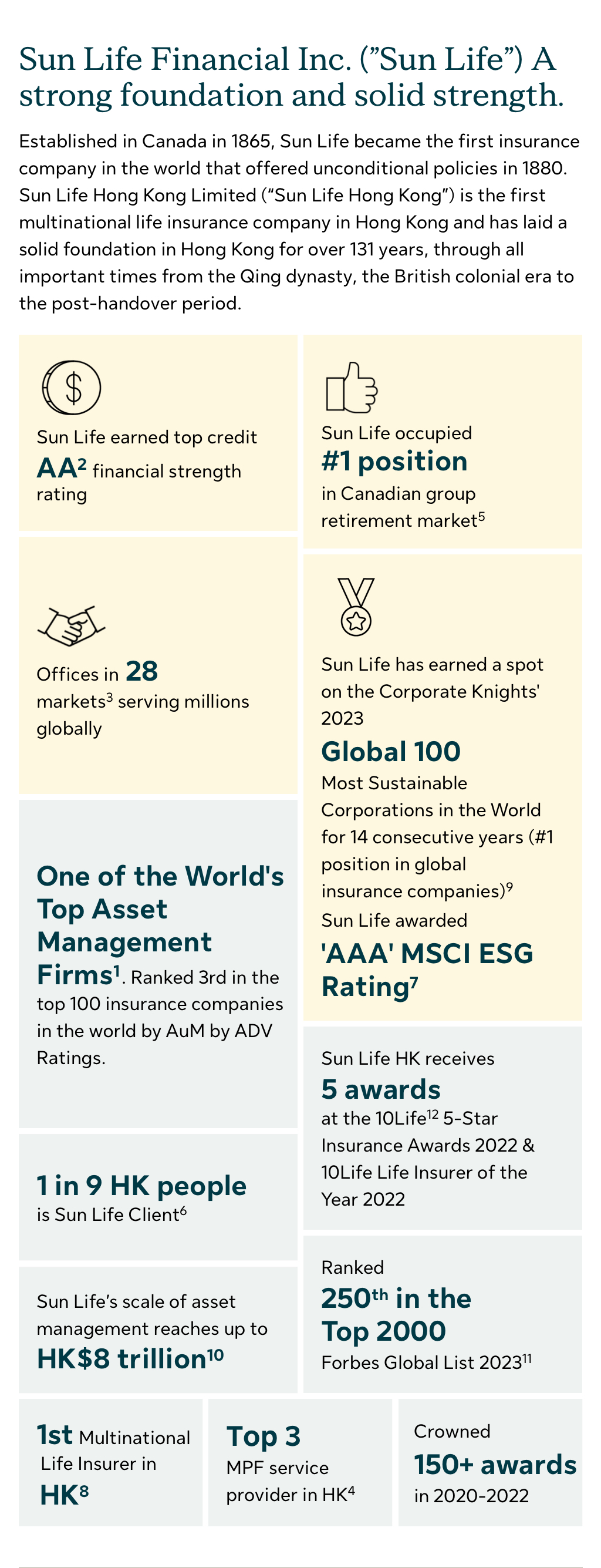

- Sun Life Financial is ranked number 32 in the top 100 asset managers in the world by Assets Under Management (AUM) by ADV Ratings, as of March 31, 2022. Source: https://www.advratings.com/top-asset-management-firms

- Ratings are for Sun Life Assurance Company of Canada.

- As of December 31, 2022

- As of September 30, 2022, including life insurance, pensions and group insurance clients.

- Fraser Pension Universe Report (based on year-end December 2020.)

- As of December 31, 2022. Based on Year 2022 Annual Report of Sun Life

- MSCI ESG as of July 31, 2023.

- Source:《厚生利群:香港保險史(1841-2008 )》, Joint Publishing HK.

- As of December 31, 2022. Based on Year 2022 Annual Report of Sun Life

- As at 31 March 2023, rounded to the nearest trillion. On a non-IFRS basis, this calculation should not be considered as a proxy under IFRS.

- Source: https://www.forbes.com/global2000./#742feb224aa2

- 10Life is a large-scale insurance comparison platform in Hong Kong, covering more than 40 insurance companies and over 1,000 life and health insurance products, allowing Hong Kong people to learn about insurance and buy the right insurance. Users can also contact 10Life's insurance consultants directly for enquiry and application.

Sun Life Hong Kong Limited ("Sun Life") has a long history of participating products. We have rich experience in managing participating accounts. Our investment experts and strong financial capabilities, together with a balanced and diversified investment portfolio, and adhere to the customer centric philosophy enable us to optimize the long-term returns for policyholders and maintain the risks at an appropriate level. On top of the guaranteed benefits, the non-guaranteed benefits would provide competitive and stable medium to long term returns:

The type of non-guaranteed dividend/bonus

The dividends or bonuses typically have the features shown in the following table. We put the interests of client first and ensure fair distribution of dividends among various groups of policyholders to protect the rights and reasonable expectations of all policyholders.

Type of dividend or bonus |

Dividend or bonus features |

Annual dividend |

|

Reversionary bonus |

Applicable to products with reversionary bonus except the policies of Foresight Deferred Annuity Plan:

Most of the on-shelf participating products of Sun Life Hong Kong are using Reversionary Bonus with some products’ cash value and face value of Reversionary Bonus are guaranteed once declared. For details, please refer to each product brochure. |

Applicable to the polices of Foresight Deferred Annuity Plan:

|

|

Terminal dividend or bonus / Special Bonus |

|

Dividends/Bonuses will typically vary based on the performance of a number of factors, with the investment return, including the impact of asset defaults and investment expenses, normally being the main determinant of bonus performance. Other factors include, but are not limited to, claims experience, taxes, expenses and policyholder persistency experience. You could press here to understand more about the dividend/bonus philosophy of Sun Life Hong Kong’s products.

How does Sun Life properly manage participating accounts to meet policyholders' expectations?

1. Strict regulatory

The projected figures of dividends/bonuses on illustration of each product have been gone through strict and meticulous calculations by forecasting the economic environment and investment returns in the next few decades. Under strict regulatory, Hong Kong insurance companies have strong business integrity and credit, and pay more attention to non-guaranteed dividends/bonuses.

External regulatory – Insurance Authority’s Guideline 16

Sun Life complies with Article 2.6 under Guideline 16 issued by Insurance Authority. The Board, on the advice of the Appointed Actuary, is ultimately responsible for interpretation of the policyholders’ reasonable expectation, and deciding the dividends/bonuses declaration, taking into account the principle of fair treatment of customers, and the issue of equity between shareholders and policyholders.

Internal regulatory

Sun Life reviews its dividend/bonus and accumulation interest rate of the policy at least once a year in accordance with the company’s dividend/bonus philosophy. Sun Life also follows the AGN9 guidelines of the Hong Kong Actuarial Society and appoints actuaries to determine best estimate assumptions with reference to past experience to determine dividends/bonuses in illustration.

2. Investment capabilities and risk management

Most participating products will invest in stocks, bonds, etc. in mature markets, and will change the investment asset allocation according to market conditions. Plans with higher guaranteed returns have a lower proportion of high-risk, high-yield assets; plans with lower guaranteed returns and higher expected returns have a higher proportion of high-risk, high-yield assets. At the same time, we will use derivatives to manage risks and add some alternative investment varieties to make the investment portfolio balanced and diversified.

3. Smoothing mechanism

Smoothing mechanism is applied to prevent dividend/bonuses would completely follow the rise and drop of investment performance in the same degree. In order to provide more stable bonuses to policyholders, the investment returns during good market conditions are actively retained as a buffer for future dividend/bonuses when the investment performance is poor, and unfavourable experience may be smoothed out over time. For products with a terminal/special bonus feature, adjustments to terminal/special bonus scales pass through experience normally with less smoothing applied.

When you purchased participating product, how to measure whether an insurance company is delivering on the projected returns on the illustration at the time of sale?

You could review below two important indicators for the performance of the product you purchased:

- You could review the overall performance by comparing the ratio of Total Cash Value in anniversary statement versus the projected Total Cash Value upon policy inception (“TCV ratio”)

- You could review fulfillment ratio to understand the overview of the historical distributed non-guaranteed amount versus the projected non-guaranteed amount at the point of sale

Important notes when reviewing the TCV ratio and fulfillment ratios:

- Savings insurance products focus on performance of long-term return. The TCV ratios and fulfillment ratios are intended for reference purpose only and should not be taken as an indicator of future performance of the participating products.

- The guaranteed and non-guaranteed ratios as well as the underlying investment strategies vary from plan to plan, and hence different plans have different investment returns. Therefore, the fulfillment ratios of plans are not directly comparable with each other, and it is recommended that financial advisors and clients should also refer to the total cash value ratio for multiple references.

- The proportion of non-guaranteed amounts distributed to premiums paid or guaranteed cash value at the beginning of the policy period is relatively low for participating products. As the proportion of non-guaranteed amounts will gradually increase over the medium- to long-term of the policy, the fulfillment ratio will then serve as an indicator for comparing the distributed amount of past dividends/bonuses with the amount in the sales illustration..

- Dividend/bonus history is not an indicator of future performance of the participating products. Thus, the fulfillment ratio can reflect only the non-guaranteed benefits declaration result for a certain past period of the policies issued; it cannot represent any future declaration plan and strategy.

The following are examples of the total cash value ratio of Sun Life’s participating products (assuming no cash value is withdrawn from the policies):

Note: The above illustrations are for reference only. The rates shown may vary from different policy (e.g., policy issue year, issue age of the insured, gender and smoking habit of the insured, etc.). The projected non-guaranteed benefits are based on the Company's bonus scales determined under a number of assumptions, including, but not limited to, current assumed investment returns (which have also incorporated the Company’s expectation of future investment returns), claims and policy terminations, and are not guaranteed. The actual amount payable may change from time to time with the values being higher or lower than those illustrated.

Before you refer to the fulfillment ratios of products, you could first understand more about the type of non-guaranteed bonus by pressing here.

What are fulfillment ratios of participating product?

In order to help policyholders understand the past performance of insurance companies in distributing non-guaranteed benefits, the "Guideline on Underwriting Long Term Insurance Business (Other Than Class C Business) (GL16)" requires insurance companies to disclose the fulfillment ratios to show the performance for non-guaranteed benefits of participating policies.

The fulfillment ratios must be disclosed for a product series for which (a) it has issued new policies since 2010, and (b) it still has policies inforce in the reporting year. Check the inforce re-projection of your policy for the latest view of the insurer on the future benefits.

If the fulfillment ratios of the product you purchased is shown as N/A, there are a number of possible reasons:

- There are no relevant in-force policies in the respective policy year. This might be because the product series was not launched yet prior to a particular calendar year; or no policies were issued during a particular calendar year; and/or no policies remain inforce by the end of the reporting year.

- The amount illustrated at point of sale was zero, so the fulfillment ratio is undetermined.

- For a terminal dividend/bonus or special bonus, the amount illustrated at the point of sale may be non-zero, but no relevant policies were terminated in the reporting year, so there are no reportable statistics.

The fulfillment ratios indicate how the non-guaranteed benefits of the policies effective in the respective year compare with the illustrated amount at the point of sale. For example, a fulfillment ratio of 120% means that the non-guaranteed benefits declared is 20% higher than the illustrated amount at the point of sale.

It should be noted that the fulfillment ratio only reflects the bonus declaration result for a certain past period of the policies issued and are intended for reference only. It does not represent any future bonus plan and strategy over a longer period for the whole policy term and should not be taken as an indicator of future bonus declaration results of the participating products.

Fulfillment Ratios are more Indicative over the Medium- to Long-Term

The proportion of non-guaranteed amounts distributed to premiums paid or guaranteed cash value at the beginning of the policy period is relatively low for participating products. As the proportion of non-guaranteed amounts will gradually increase over the medium- to long-term of the policy, the fulfillment ratio will then serve as an indicator for the reference amount for comparing the amount of past dividends/bonuses distributed with the sales.

Fulfillment ratios for policies with Annual Dividend

The fulfillment ratio for annual dividends is calculated as the ratio of aggregate actual accumulated non-guaranteed annual dividends (including actual dividend accumulation interest but excluding terminal dividends, if applicable) against the aggregate illustrated amounts for non-guaranteed annual dividends provided to customers at the point of sale, for all relevant inforce policies.

For the purpose of calculation of fulfillment ratios, it is assumed that policyholders opted to leave all declared dividends with the Company for interest accumulation based on the relevant actual interest rates. For products offering non-guaranteed monthly incomes, all non-guaranteed components of policies are included in calculation of fulfillment ratios (e.g. accumulated dividends during accumulation phase, accumulated non-guaranteed interests on guaranteed monthly incomes left on deposit, etc.). It is also assumed that policyholders opted to leave all monthly incomes with the Company for interest accumulation based on the relevant actual interest rates.

Fulfillment ratios for policies with Reversionary Bonus

The fulfillment ratio for reversionary bonuses is calculated as the ratio of the aggregate actual accumulated non-guaranteed reversionary bonuses (excluding terminal bonuses or special bonuses, if applicable) against the aggregate illustrated amounts for non-guaranteed reversionary bonuses provided to customers at the point of sale, for all relevant inforce policies and all relevant policies terminated in the reporting year. For the purpose of calculation of fulfillment ratios, cash value of reversionary bonuses is used in the calculation.

Fulfillment ratios for policies with terminal dividends/bonuses or special bonuses

The fulfillment ratio for terminal dividends/bonuses or special bonuses is calculated as the ratio of the aggregate payout of non-guaranteed terminal dividends/bonuses or special bonuses (if applicable) against the aggregate illustrated amounts for non-guaranteed terminal dividends/bonuses or special bonuses provided to customers at the point of sale, for all relevant policies terminated in the reporting year.. For the purpose of calculation of fulfillment ratios, cash value of terminal dividends/bonuses or special bonuses is used in the calculation.

Please note the figures in below tables are calculated based on the data as of relevant reporting year and have been rounded to the nearest percent.

The following tables show the non-guaranteed dividends/bonuses fulfillment ratios for each product series which has new policies issued by Sun Life Hong Kong Limited (the "Company") since 2010 and still has policies inforce in the current reporting year. The fulfillment ratio is calculated as the average ratio of non-guaranteed dividends/bonuses actually declared/paid against the illustrated amounts at the point of sale. Fulfillment ratios are for reference only, dividend/bonus history is not an indicator of future declaration/performance of the participating products.

Products with the same features but with different pricing information (e.g. with different level of guaranteed and non-guaranteed benefit, premium rate, etc.) or different policy currency may be grouped into the same product series if differences in fulfillment ratios are considered immaterial. The disclosed fulfillment ratios are for basic plans only and all relevant policies are included in the calculation. In addition, to be consistent with the illustration basis, the actual amounts are calculated up to the respective policy anniversary.

Fulfillment Ratios for Reversionary Bonuses for Reporting Year 2023 of respective products

| Product | Product Type | Policy Year 1 (policies effective in 2022) | Policy Year 2 (policies effective in 2021) | Policy Year 3 (policies effective in 2020) | Policy Year 4 (policies effective in 2019) | Policy Year 5 (policies effective in 2018) | Policy Year 6 (policies effective in 2017) | Policy Year 7 (policies effective in 2016) | Policy Year 8 (policies effective in 2015) | Policy Year 9 (policies effective in 2014) | Policy Year 10 (policies effective in 2013) | Policy Year 10+ (policies effective in 2010 - 2012) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Venus1 | Participating Whole Life | Closed to sales | 100% | 100% | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched |

1This product is closed to new business.

Fulfillment Ratios for Terminal Dividends/Bonuses or Special Bonuses for Reporting Year 2023 of respective products

| Product | Product Type | Policy Year 1 (policies effective in 2022) | Policy Year 2 (policies effective in 2021) | Policy Year 3 (policies effective in 2020) | Policy Year 4 (policies effective in 2019) | Policy Year 5 (policies effective in 2018) | Policy Year 6 (policies effective in 2017) | Policy Year 7 (policies effective in 2016) | Policy Year 8 (policies effective in 2015) | Policy Year 9 (policies effective in 2014) | Policy Year 10 (policies effective in 2013) | Policy Year 10+ (policies effective in 2010 - 2012) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Venus 1 | Participating Whole Life | Closed to sales | NA | NA | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched |

1This product is closed to new business.

Remarks:

Some of the above fulfillment ratios may show "N/A" (not applicable) due to one or more of the following reasons:

1.No relevant policies for the respective policy year because:

- -no policies were issued during a particular calendar year; and/or

- -no policies remain inforce by the end of the reporting year.

2.No annual dividends or reversionary bonuses were entitled by the relevant policies up to the respective policy year.

3.There were no actual payouts of terminal dividends/bonuses or special bonuses for the respective policy year because:

- -no terminal dividends/bonuses or special bonuses were entitled by the relevant policies up to the respective policy year; or

- -there were no terminations and/or other applicable events triggering the actual payouts of terminal dividends/bonuses or special bonuses in the reporting year for the relevant policies.

The following tables show the non-guaranteed dividends/bonuses fulfillment ratios for each product series which has new policies issued by Sun Life Hong Kong Limited (the "Company") since 2010 and still has policies inforce in the current reporting year. The fulfillment ratio is calculated as the average ratio of non-guaranteed dividends/bonuses actually declared/paid against the illustrated amounts at the point of sale. Fulfillment ratios are for reference only, dividend/bonus history is not an indicator of future declaration/performance of the participating products.

Products with the same features but with different pricing information (e.g. with different level of guaranteed and non-guaranteed benefit, premium rate, etc.) or different policy currency may be grouped into the same product series if differences in fulfillment ratios are considered immaterial. The disclosed fulfillment ratios are for basic plans only and all relevant policies are included in the calculation. In addition, to be consistent with the illustration basis, the actual amounts are calculated up to the respective policy anniversary.

Fulfillment Ratios for Annual Dividends for Reporting Year 2023 of respective products

| Product | Product Type | Policy Year 1 (policies effective in 2022) | Policy Year 2 (policies effective in 2021) | Policy Year 3 (policies effective in 2020) | Policy Year 4 (policies effective in 2019) | Policy Year 5 (policies effective in 2018) | Policy Year 6 (policies effective in 2017) | Policy Year 7 (policies effective in 2016) | Policy Year 8 (policies effective in 2015) | Policy Year 9 (policies effective in 2014) | Policy Year 10 (policies effective in 2013) | Policy Year 10+ (policies effective in 2010 - 2012) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| LIFE Super1 , LIFE Super Plus1 | Participating Whole Life | Closed to sales | Closed to sales | 98% | 98% | 98% | 97% | 97% | 97% | 99% | 109% | 95% |

1This product is closed to new business.

Remarks:

Some of the above fulfillment ratios may show "N/A" (not applicable) due to one or more of the following reasons:

1.No relevant policies for the respective policy year because:

- -no policies were issued during a particular calendar year; and/or

- -no policies remain inforce by the end of the reporting year.

2.No annual dividends or reversionary bonuses were entitled by the relevant policies up to the respective policy year.

3.There were no actual payouts of terminal dividends/bonuses or special bonuses for the respective policy year because:

- -no terminal dividends/bonuses or special bonuses were entitled by the relevant policies up to the respective policy year; or

- -there were no terminations and/or other applicable events triggering the actual payouts of terminal dividends/bonuses or special bonuses in the reporting year for the relevant policies.

The following tables show the non-guaranteed dividends/bonuses fulfillment ratios for each product series which has new policies issued by Sun Life Hong Kong Limited (the "Company") since 2010 and still has policies inforce in the current reporting year. The fulfillment ratio is calculated as the average ratio of non-guaranteed dividends/bonuses actually declared/paid against the illustrated amounts at the point of sale. Fulfillment ratios are for reference only, dividend/bonus history is not an indicator of future declaration/performance of the participating products.

Products with the same features but with different pricing information (e.g. with different level of guaranteed and non-guaranteed benefit, premium rate, etc.) or different policy currency may be grouped into the same product series if differences in fulfillment ratios are considered immaterial. The disclosed fulfillment ratios are for basic plans only and all relevant policies are included in the calculation. In addition, to be consistent with the illustration basis, the actual amounts are calculated up to the respective policy anniversary.

Fulfillment Ratios for Annual Dividends for Reporting Year 2023 of respective products

| Product | Product Type | Policy Year 1 (policies effective in 2022) | Policy Year 2 (policies effective in 2021) | Policy Year 3 (policies effective in 2020) | Policy Year 4 (policies effective in 2019) | Policy Year 5 (policies effective in 2018) | Policy Year 6 (policies effective in 2017) | Policy Year 7 (policies effective in 2016) | Policy Year 8 (policies effective in 2015) | Policy Year 9 (policies effective in 2014) | Policy Year 10 (policies effective in 2013) | Policy Year 10+ (policies effective in 2010 - 2012) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Vision | Participating Whole Life | NA | 98% | 98% | 98% | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched |

Fulfillment Ratios for Reversionary Bonuses for Reporting Year 2023 of respective products

| Product | Product Type | Policy Year 1 (policies effective in 2022) | Policy Year 2 (policies effective in 2021) | Policy Year 3 (policies effective in 2020) | Policy Year 4 (policies effective in 2019) | Policy Year 5 (policies effective in 2018) | Policy Year 6 (policies effective in 2017) | Policy Year 7 (policies effective in 2016) | Policy Year 8 (policies effective in 2015) | Policy Year 9 (policies effective in 2014) | Policy Year 10 (policies effective in 2013) | Policy Year 10+ (policies effective in 2010 - 2012) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Vision | Participating Whole Life | 100% | 98% | 94% | 91% | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched |

Fulfillment Ratios for Terminal Dividends/Bonuses or Special Bonuses for Reporting Year 2023 of respective products

| Product | Product Type | Policy Year 1 (policies effective in 2022) | Policy Year 2 (policies effective in 2021) | Policy Year 3 (policies effective in 2020) | Policy Year 4 (policies effective in 2019) | Policy Year 5 (policies effective in 2018) | Policy Year 6 (policies effective in 2017) | Policy Year 7 (policies effective in 2016) | Policy Year 8 (policies effective in 2015) | Policy Year 9 (policies effective in 2014) | Policy Year 10 (policies effective in 2013) | Policy Year 10+ (policies effective in 2010 - 2012) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Vision | Participating Whole Life | NA | NA | NA | NA | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched |

Remarks:

Some of the above fulfillment ratios may show "N/A" (not applicable) due to one or more of the following reasons:

1.No relevant policies for the respective policy year because:

- -no policies were issued during a particular calendar year; and/or

- -no policies remain inforce by the end of the reporting year.

2.No annual dividends or reversionary bonuses were entitled by the relevant policies up to the respective policy year.

3.There were no actual payouts of terminal dividends/bonuses or special bonuses for the respective policy year because:

- -no terminal dividends/bonuses or special bonuses were entitled by the relevant policies up to the respective policy year; or

- -there were no terminations and/or other applicable events triggering the actual payouts of terminal dividends/bonuses or special bonuses in the reporting year for the relevant policies.

The following tables show the non-guaranteed dividends/bonuses fulfillment ratios for each product series which has new policies issued by Sun Life Hong Kong Limited (the "Company") since 2010 and still has policies inforce in the current reporting year. The fulfillment ratio is calculated as the average ratio of non-guaranteed dividends/bonuses actually declared/paid against the illustrated amounts at the point of sale. Fulfillment ratios are for reference only, dividend/bonus history is not an indicator of future declaration/performance of the participating products.

Products with the same features but with different pricing information (e.g. with different level of guaranteed and non-guaranteed benefit, premium rate, etc.) or different policy currency may be grouped into the same product series if differences in fulfillment ratios are considered immaterial. The disclosed fulfillment ratios are for basic plans only and all relevant policies are included in the calculation. In addition, to be consistent with the illustration basis, the actual amounts are calculated up to the respective policy anniversary.

Fulfillment Ratios for Reversionary Bonuses for Reporting Year 2023 of respective products

| Product | Product Type | Policy Year 1 (policies effective in 2022) | Policy Year 2 (policies effective in 2021) | Policy Year 3 (policies effective in 2020) | Policy Year 4 (policies effective in 2019) | Policy Year 5 (policies effective in 2018) | Policy Year 6 (policies effective in 2017) | Policy Year 7 (policies effective in 2016) | Policy Year 8 (policies effective in 2015) | Policy Year 9 (policies effective in 2014) | Policy Year 10 (policies effective in 2013) | Policy Year 10+ (policies effective in 2010 - 2012) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Generations 1 | Participating Whole Life | Closed to sales | 96% | 91% | 93% | 94% | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched |

1This product is closed to new business.

Fulfillment Ratios for Terminal Dividends/Bonuses or Special Bonuses for Reporting Year 2023 of respective products

| Product | Product Type | Policy Year 1 (policies effective in 2022) | Policy Year 2 (policies effective in 2021) | Policy Year 3 (policies effective in 2020) | Policy Year 4 (policies effective in 2019) | Policy Year 5 (policies effective in 2018) | Policy Year 6 (policies effective in 2017) | Policy Year 7 (policies effective in 2016) | Policy Year 8 (policies effective in 2015) | Policy Year 9 (policies effective in 2014) | Policy Year 10 (policies effective in 2013) | Policy Year 10+ (policies effective in 2010 - 2012) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Generations 1 | Participating Whole Life | Closed to sales | NA | NA | NA | NA | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched |

1This product is closed to new business.

Remarks:

Some of the above fulfillment ratios may show "N/A" (not applicable) due to one or more of the following reasons:

1.No relevant policies for the respective policy year because:

- -no policies were issued during a particular calendar year; and/or

- -no policies remain inforce by the end of the reporting year.

2.No annual dividends or reversionary bonuses were entitled by the relevant policies up to the respective policy year.

3.There were no actual payouts of terminal dividends/bonuses or special bonuses for the respective policy year because:

- -no terminal dividends/bonuses or special bonuses were entitled by the relevant policies up to the respective policy year; or

- -there were no terminations and/or other applicable events triggering the actual payouts of terminal dividends/bonuses or special bonuses in the reporting year for the relevant policies.

The following tables show the non-guaranteed dividends/bonuses fulfillment ratios for each product series which has new policies issued by Sun Life Hong Kong Limited (the "Company") since 2010 and still has policies inforce in the current reporting year. The fulfillment ratio is calculated as the average ratio of non-guaranteed dividends/bonuses actually declared/paid against the illustrated amounts at the point of sale. Fulfillment ratios are for reference only, dividend/bonus history is not an indicator of future declaration/performance of the participating products.

Products with the same features but with different pricing information (e.g. with different level of guaranteed and non-guaranteed benefit, premium rate, etc.) or different policy currency may be grouped into the same product series if differences in fulfillment ratios are considered immaterial. The disclosed fulfillment ratios are for basic plans only and all relevant policies are included in the calculation. In addition, to be consistent with the illustration basis, the actual amounts are calculated up to the respective policy anniversary.

Fulfillment Ratios for Reversionary Bonuses for Reporting Year 2023 of respective products

| Product | Product Type | Policy Year 1 (policies effective in 2022) | Policy Year 2 (policies effective in 2021) | Policy Year 3 (policies effective in 2020) | Policy Year 4 (policies effective in 2019) | Policy Year 5 (policies effective in 2018) | Policy Year 6 (policies effective in 2017) | Policy Year 7 (policies effective in 2016) | Policy Year 8 (policies effective in 2015) | Policy Year 9 (policies effective in 2014) | Policy Year 10 (policies effective in 2013) | Policy Year 10+ (policies effective in 2010 - 2012) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Victory | Participating Whole Life | NA | NA | 110% | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched |

Fulfillment Ratios for Terminal Dividends/Bonuses or Special Bonuses for Reporting Year 2023 of respective products

| Product | Product Type | Policy Year 1 (policies effective in 2022) | Policy Year 2 (policies effective in 2021) | Policy Year 3 (policies effective in 2020) | Policy Year 4 (policies effective in 2019) | Policy Year 5 (policies effective in 2018) | Policy Year 6 (policies effective in 2017) | Policy Year 7 (policies effective in 2016) | Policy Year 8 (policies effective in 2015) | Policy Year 9 (policies effective in 2014) | Policy Year 10 (policies effective in 2013) | Policy Year 10+ (policies effective in 2010 - 2012) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Victory | Participating Whole Life | NA | NA | NA | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched |

Remarks:

Some of the above fulfillment ratios may show "N/A" (not applicable) due to one or more of the following reasons:

1.No relevant policies for the respective policy year because:

- -no policies were issued during a particular calendar year; and/or

- -no policies remain inforce by the end of the reporting year.

2.No annual dividends or reversionary bonuses were entitled by the relevant policies up to the respective policy year.

3.There were no actual payouts of terminal dividends/bonuses or special bonuses for the respective policy year because:

- -no terminal dividends/bonuses or special bonuses were entitled by the relevant policies up to the respective policy year; or

- -there were no terminations and/or other applicable events triggering the actual payouts of terminal dividends/bonuses or special bonuses in the reporting year for the relevant policies.

The following tables show the non-guaranteed dividends/bonuses fulfillment ratios for each product series which has new policies issued by Sun Life Hong Kong Limited (the "Company") since 2010 and still has policies inforce in the current reporting year. The fulfillment ratio is calculated as the average ratio of non-guaranteed dividends/bonuses actually declared/paid against the illustrated amounts at the point of sale. Fulfillment ratios are for reference only, dividend/bonus history is not an indicator of future declaration/performance of the participating products.

Products with the same features but with different pricing information (e.g. with different level of guaranteed and non-guaranteed benefit, premium rate, etc.) or different policy currency may be grouped into the same product series if differences in fulfillment ratios are considered immaterial. The disclosed fulfillment ratios are for basic plans only and all relevant policies are included in the calculation. In addition, to be consistent with the illustration basis, the actual amounts are calculated up to the respective policy anniversary.

Fulfillment Ratios for Annual Dividends for Reporting Year 2023 of respective products

| Product | Product Type | Policy Year 1 (policies effective in 2022) | Policy Year 2 (policies effective in 2021) | Policy Year 3 (policies effective in 2020) | Policy Year 4 (policies effective in 2019) | Policy Year 5 (policies effective in 2018) | Policy Year 6 (policies effective in 2017) | Policy Year 7 (policies effective in 2016) | Policy Year 8 (policies effective in 2015) | Policy Year 9 (policies effective in 2014) | Policy Year 10 (policies effective in 2013) | Policy Year 10+ (policies effective in 2010 - 2012) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| HOPE Educator 1 | Participating Whole Life | Closed to sales | Closed to sales | 76% | 89% | 88% | 84% | 88% | 91% | 92% | 93% | 89% |

1This product is closed to new business.

Remarks:

Some of the above fulfillment ratios may show "N/A" (not applicable) due to one or more of the following reasons:

1.No relevant policies for the respective policy year because:

- -no policies were issued during a particular calendar year; and/or

- -no policies remain inforce by the end of the reporting year.

2.No annual dividends or reversionary bonuses were entitled by the relevant policies up to the respective policy year.

3.There were no actual payouts of terminal dividends/bonuses or special bonuses for the respective policy year because:

- -no terminal dividends/bonuses or special bonuses were entitled by the relevant policies up to the respective policy year; or

- -there were no terminations and/or other applicable events triggering the actual payouts of terminal dividends/bonuses or special bonuses in the reporting year for the relevant policies.

The following tables show the non-guaranteed dividends/bonuses fulfillment ratios for each product series which has new policies issued by Sun Life Hong Kong Limited (the "Company") since 2010 and still has policies inforce in the current reporting year. The fulfillment ratio is calculated as the average ratio of non-guaranteed dividends/bonuses actually declared/paid against the illustrated amounts at the point of sale. Fulfillment ratios are for reference only, dividend/bonus history is not an indicator of future declaration/performance of the participating products.

Products with the same features but with different pricing information (e.g. with different level of guaranteed and non-guaranteed benefit, premium rate, etc.) or different policy currency may be grouped into the same product series if differences in fulfillment ratios are considered immaterial. The disclosed fulfillment ratios are for basic plans only and all relevant policies are included in the calculation. In addition, to be consistent with the illustration basis, the actual amounts are calculated up to the respective policy anniversary.

Fulfillment Ratios for Reversionary Bonuses for Reporting Year 2023 of respective products

| Product | Product Type | Policy Year 1 (policies effective in 2022) | Policy Year 2 (policies effective in 2021) | Policy Year 3 (policies effective in 2020) | Policy Year 4 (policies effective in 2019) | Policy Year 5 (policies effective in 2018) | Policy Year 6 (policies effective in 2017) | Policy Year 7 (policies effective in 2016) | Policy Year 8 (policies effective in 2015) | Policy Year 9 (policies effective in 2014) | Policy Year 10 (policies effective in 2013) | Policy Year 10+ (policies effective in 2010 - 2012) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Commitment 1 | Participating Whole Life | 100% | 91% | 86% | 88% | 87% | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched |

1This product is closed to new business.

Fulfillment Ratios for Terminal Dividends/Bonuses or Special Bonuses for Reporting Year 2023 of respective products

| Product | Product Type | Policy Year 1 (policies effective in 2022) | Policy Year 2 (policies effective in 2021) | Policy Year 3 (policies effective in 2020) | Policy Year 4 (policies effective in 2019) | Policy Year 5 (policies effective in 2018) | Policy Year 6 (policies effective in 2017) | Policy Year 7 (policies effective in 2016) | Policy Year 8 (policies effective in 2015) | Policy Year 9 (policies effective in 2014) | Policy Year 10 (policies effective in 2013) | Policy Year 10+ (policies effective in 2010 - 2012) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Commitment 1 | Participating Whole Life | NA | NA | NA | NA | NA | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched |

1This product is closed to new business.

Remarks:

Some of the above fulfillment ratios may show "N/A" (not applicable) due to one or more of the following reasons:

1.No relevant policies for the respective policy year because:

- -no policies were issued during a particular calendar year; and/or

- -no policies remain inforce by the end of the reporting year.

2.No annual dividends or reversionary bonuses were entitled by the relevant policies up to the respective policy year.

3.There were no actual payouts of terminal dividends/bonuses or special bonuses for the respective policy year because:

- -no terminal dividends/bonuses or special bonuses were entitled by the relevant policies up to the respective policy year; or

- -there were no terminations and/or other applicable events triggering the actual payouts of terminal dividends/bonuses or special bonuses in the reporting year for the relevant policies.

The following tables show the non-guaranteed dividends/bonuses fulfillment ratios for each product series which has new policies issued by Sun Life Hong Kong Limited (the "Company") since 2010 and still has policies inforce in the current reporting year. The fulfillment ratio is calculated as the average ratio of non-guaranteed dividends/bonuses actually declared/paid against the illustrated amounts at the point of sale. Fulfillment ratios are for reference only, dividend/bonus history is not an indicator of future declaration/performance of the participating products.

Products with the same features but with different pricing information (e.g. with different level of guaranteed and non-guaranteed benefit, premium rate, etc.) or different policy currency may be grouped into the same product series if differences in fulfillment ratios are considered immaterial. The disclosed fulfillment ratios are for basic plans only and all relevant policies are included in the calculation. In addition, to be consistent with the illustration basis, the actual amounts are calculated up to the respective policy anniversary.

Fulfillment Ratios for Reversionary Bonuses for Reporting Year 2023 of respective products

| Product | Product Type | Policy Year 1 (policies effective in 2022) | Policy Year 2 (policies effective in 2021) | Policy Year 3 (policies effective in 2020) | Policy Year 4 (policies effective in 2019) | Policy Year 5 (policies effective in 2018) | Policy Year 6 (policies effective in 2017) | Policy Year 7 (policies effective in 2016) | Policy Year 8 (policies effective in 2015) | Policy Year 9 (policies effective in 2014) | Policy Year 10 (policies effective in 2013) | Policy Year 10+ (policies effective in 2010 - 2012) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Generations II | Participating Whole Life | NA | NA | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched |

Fulfillment Ratios for Terminal Dividends/Bonuses or Special Bonuses for Reporting Year 2023 of respective products

| Product | Product Type | Policy Year 1 (policies effective in 2022) | Policy Year 2 (policies effective in 2021) | Policy Year 3 (policies effective in 2020) | Policy Year 4 (policies effective in 2019) | Policy Year 5 (policies effective in 2018) | Policy Year 6 (policies effective in 2017) | Policy Year 7 (policies effective in 2016) | Policy Year 8 (policies effective in 2015) | Policy Year 9 (policies effective in 2014) | Policy Year 10 (policies effective in 2013) | Policy Year 10+ (policies effective in 2010 - 2012) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Generations II | Participating Whole Life | NA | NA | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched |

Remarks:

Some of the above fulfillment ratios may show "N/A" (not applicable) due to one or more of the following reasons:

1.No relevant policies for the respective policy year because:

- -no policies were issued during a particular calendar year; and/or

- -no policies remain inforce by the end of the reporting year.

2.No annual dividends or reversionary bonuses were entitled by the relevant policies up to the respective policy year.

3.There were no actual payouts of terminal dividends/bonuses or special bonuses for the respective policy year because:

- -no terminal dividends/bonuses or special bonuses were entitled by the relevant policies up to the respective policy year; or

- -there were no terminations and/or other applicable events triggering the actual payouts of terminal dividends/bonuses or special bonuses in the reporting year for the relevant policies.

The following tables show the non-guaranteed dividends/bonuses fulfillment ratios for each product series which has new policies issued by Sun Life Hong Kong Limited (the "Company") since 2010 and still has policies inforce in the current reporting year. The fulfillment ratio is calculated as the average ratio of non-guaranteed dividends/bonuses actually declared/paid against the illustrated amounts at the point of sale. Fulfillment ratios are for reference only, dividend/bonus history is not an indicator of future declaration/performance of the participating products.

Products with the same features but with different pricing information (e.g. with different level of guaranteed and non-guaranteed benefit, premium rate, etc.) or different policy currency may be grouped into the same product series if differences in fulfillment ratios are considered immaterial. The disclosed fulfillment ratios are for basic plans only and all relevant policies are included in the calculation. In addition, to be consistent with the illustration basis, the actual amounts are calculated up to the respective policy anniversary.

Fulfillment Ratios for Reversionary Bonuses for Reporting Year 2023 of respective products

| Product | Product Type | Policy Year 1 (policies effective in 2022) | Policy Year 2 (policies effective in 2021) | Policy Year 3 (policies effective in 2020) | Policy Year 4 (policies effective in 2019) | Policy Year 5 (policies effective in 2018) | Policy Year 6 (policies effective in 2017) | Policy Year 7 (policies effective in 2016) | Policy Year 8 (policies effective in 2015) | Policy Year 9 (policies effective in 2014) | Policy Year 10 (policies effective in 2013) | Policy Year 10+ (policies effective in 2010 - 2012) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Life Brilliance | Participating Whole Life | NA | NA | 92% | 87% | 89% | 90% | 83% | 83% | 83% | 87% | Not yet launched |

Fulfillment Ratios for Terminal Dividends/Bonuses or Special Bonuses for Reporting Year 2023 of respective products

| Product | Product Type | Policy Year 1 (policies effective in 2022) | Policy Year 2 (policies effective in 2021) | Policy Year 3 (policies effective in 2020) | Policy Year 4 (policies effective in 2019) | Policy Year 5 (policies effective in 2018) | Policy Year 6 (policies effective in 2017) | Policy Year 7 (policies effective in 2016) | Policy Year 8 (policies effective in 2015) | Policy Year 9 (policies effective in 2014) | Policy Year 10 (policies effective in 2013) | Policy Year 10+ (policies effective in 2010 - 2012) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Life Brilliance | Participating Whole Life | NA | NA | NA | NA | NA | NA | NA | NA | NA | NA | Not yet launched |

Remarks:

Some of the above fulfillment ratios may show "N/A" (not applicable) due to one or more of the following reasons:

1.No relevant policies for the respective policy year because:

- -no policies were issued during a particular calendar year; and/or

- -no policies remain inforce by the end of the reporting year.

2.No annual dividends or reversionary bonuses were entitled by the relevant policies up to the respective policy year.

3.There were no actual payouts of terminal dividends/bonuses or special bonuses for the respective policy year because:

- -no terminal dividends/bonuses or special bonuses were entitled by the relevant policies up to the respective policy year; or

- -there were no terminations and/or other applicable events triggering the actual payouts of terminal dividends/bonuses or special bonuses in the reporting year for the relevant policies.

The following tables show the non-guaranteed dividends/bonuses fulfillment ratios for each product series which has new policies issued by Sun Life Hong Kong Limited (the "Company") since 2010 and still has policies inforce in the current reporting year. The fulfillment ratio is calculated as the average ratio of non-guaranteed dividends/bonuses actually declared/paid against the illustrated amounts at the point of sale. Fulfillment ratios are for reference only, dividend/bonus history is not an indicator of future declaration/performance of the participating products.

Products with the same features but with different pricing information (e.g. with different level of guaranteed and non-guaranteed benefit, premium rate, etc.) or different policy currency may be grouped into the same product series if differences in fulfillment ratios are considered immaterial. The disclosed fulfillment ratios are for basic plans only and all relevant policies are included in the calculation. In addition, to be consistent with the illustration basis, the actual amounts are calculated up to the respective policy anniversary.

Fulfillment Ratios for Reversionary Bonuses for Reporting Year 2023 of respective products

| Product | Product Type | Policy Year 1 (policies effective in 2022) | Policy Year 2 (policies effective in 2021) | Policy Year 3 (policies effective in 2020) | Policy Year 4 (policies effective in 2019) | Policy Year 5 (policies effective in 2018) | Policy Year 6 (policies effective in 2017) | Policy Year 7 (policies effective in 2016) | Policy Year 8 (policies effective in 2015) | Policy Year 9 (policies effective in 2014) | Policy Year 10 (policies effective in 2013) | Policy Year 10+ (policies effective in 2010 - 2012) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Prosperity 1 | Participating Whole Life | Closed to sales | 91% | 89% | 92% | 93% | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched |

1This product is closed to new business.

Fulfillment Ratios for Terminal Dividends/Bonuses or Special Bonuses for Reporting Year 2023 of respective products

| Product | Product Type | Policy Year 1 (policies effective in 2022) | Policy Year 2 (policies effective in 2021) | Policy Year 3 (policies effective in 2020) | Policy Year 4 (policies effective in 2019) | Policy Year 5 (policies effective in 2018) | Policy Year 6 (policies effective in 2017) | Policy Year 7 (policies effective in 2016) | Policy Year 8 (policies effective in 2015) | Policy Year 9 (policies effective in 2014) | Policy Year 10 (policies effective in 2013) | Policy Year 10+ (policies effective in 2010 - 2012) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Prosperity 1 | Participating Whole Life | Closed to sales | NA | NA | NA | NA | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched |

1This product is closed to new business.

Remarks:

Some of the above fulfillment ratios may show "N/A" (not applicable) due to one or more of the following reasons:

1.No relevant policies for the respective policy year because:

- -no policies were issued during a particular calendar year; and/or

- -no policies remain inforce by the end of the reporting year.

2.No annual dividends or reversionary bonuses were entitled by the relevant policies up to the respective policy year.

3.There were no actual payouts of terminal dividends/bonuses or special bonuses for the respective policy year because:

- -no terminal dividends/bonuses or special bonuses were entitled by the relevant policies up to the respective policy year; or

- -there were no terminations and/or other applicable events triggering the actual payouts of terminal dividends/bonuses or special bonuses in the reporting year for the relevant policies.

The following tables show the non-guaranteed dividends/bonuses fulfillment ratios for each product series which has new policies issued by Sun Life Hong Kong Limited (the "Company") since 2010 and still has policies inforce in the current reporting year. The fulfillment ratio is calculated as the average ratio of non-guaranteed dividends/bonuses actually declared/paid against the illustrated amounts at the point of sale. Fulfillment ratios are for reference only, dividend/bonus history is not an indicator of future declaration/performance of the participating products.

Products with the same features but with different pricing information (e.g. with different level of guaranteed and non-guaranteed benefit, premium rate, etc.) or different policy currency may be grouped into the same product series if differences in fulfillment ratios are considered immaterial. The disclosed fulfillment ratios are for basic plans only and all relevant policies are included in the calculation. In addition, to be consistent with the illustration basis, the actual amounts are calculated up to the respective policy anniversary.

Fulfillment Ratios for Reversionary Bonuses for Reporting Year 2023 of respective products

| Product | Product Type | Policy Year 1 (policies effective in 2022) | Policy Year 2 (policies effective in 2021) | Policy Year 3 (policies effective in 2020) | Policy Year 4 (policies effective in 2019) | Policy Year 5 (policies effective in 2018) | Policy Year 6 (policies effective in 2017) | Policy Year 7 (policies effective in 2016) | Policy Year 8 (policies effective in 2015) | Policy Year 9 (policies effective in 2014) | Policy Year 10 (policies effective in 2013) | Policy Year 10+ (policies effective in 2010 - 2012) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Stellar 1 | Participating Whole Life | NA | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched |

1This product is closed to new business.

Fulfillment Ratios for Terminal Dividends/Bonuses or Special Bonuses for Reporting Year 2023 of respective products

| Product | Product Type | Policy Year 1 (policies effective in 2022) | Policy Year 2 (policies effective in 2021) | Policy Year 3 (policies effective in 2020) | Policy Year 4 (policies effective in 2019) | Policy Year 5 (policies effective in 2018) | Policy Year 6 (policies effective in 2017) | Policy Year 7 (policies effective in 2016) | Policy Year 8 (policies effective in 2015) | Policy Year 9 (policies effective in 2014) | Policy Year 10 (policies effective in 2013) | Policy Year 10+ (policies effective in 2010 - 2012) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Stellar 1 | Participating Whole Life | NA | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched |

1This product is closed to new business.

Remarks:

Some of the above fulfillment ratios may show "N/A" (not applicable) due to one or more of the following reasons:

1.No relevant policies for the respective policy year because:

- -no policies were issued during a particular calendar year; and/or

- -no policies remain inforce by the end of the reporting year.

2.No annual dividends or reversionary bonuses were entitled by the relevant policies up to the respective policy year.

3.There were no actual payouts of terminal dividends/bonuses or special bonuses for the respective policy year because:

- -no terminal dividends/bonuses or special bonuses were entitled by the relevant policies up to the respective policy year; or

- -there were no terminations and/or other applicable events triggering the actual payouts of terminal dividends/bonuses or special bonuses in the reporting year for the relevant policies.

The following tables show the non-guaranteed dividends/bonuses fulfillment ratios for each product series which has new policies issued by Sun Life Hong Kong Limited (the "Company") since 2010 and still has policies inforce in the current reporting year. The fulfillment ratio is calculated as the average ratio of non-guaranteed dividends/bonuses actually declared/paid against the illustrated amounts at the point of sale. Fulfillment ratios are for reference only, dividend/bonus history is not an indicator of future declaration/performance of the participating products.

Products with the same features but with different pricing information (e.g. with different level of guaranteed and non-guaranteed benefit, premium rate, etc.) or different policy currency may be grouped into the same product series if differences in fulfillment ratios are considered immaterial. The disclosed fulfillment ratios are for basic plans only and all relevant policies are included in the calculation. In addition, to be consistent with the illustration basis, the actual amounts are calculated up to the respective policy anniversary.

Fulfillment Ratios for Reversionary Bonuses for Reporting Year 2023 of respective products

| Product | Product Type | Policy Year 1 (policies effective in 2022) | Policy Year 2 (policies effective in 2021) | Policy Year 3 (policies effective in 2020) | Policy Year 4 (policies effective in 2019) | Policy Year 5 (policies effective in 2018) | Policy Year 6 (policies effective in 2017) | Policy Year 7 (policies effective in 2016) | Policy Year 8 (policies effective in 2015) | Policy Year 9 (policies effective in 2014) | Policy Year 10 (policies effective in 2013) | Policy Year 10+ (policies effective in 2010 - 2012) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| SunGift | Participating Whole Life | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched |

Fulfillment Ratios for Terminal Dividends/Bonuses or Special Bonuses for Reporting Year 2023 of respective products

| Product | Product Type | Policy Year 1 (policies effective in 2022) | Policy Year 2 (policies effective in 2021) | Policy Year 3 (policies effective in 2020) | Policy Year 4 (policies effective in 2019) | Policy Year 5 (policies effective in 2018) | Policy Year 6 (policies effective in 2017) | Policy Year 7 (policies effective in 2016) | Policy Year 8 (policies effective in 2015) | Policy Year 9 (policies effective in 2014) | Policy Year 10 (policies effective in 2013) | Policy Year 10+ (policies effective in 2010 - 2012) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| SunGift | Participating Whole Life | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched |

Remarks:

Some of the above fulfillment ratios may show "N/A" (not applicable) due to one or more of the following reasons:

1.No relevant policies for the respective policy year because:

- -no policies were issued during a particular calendar year; and/or

- -no policies remain inforce by the end of the reporting year.

2.No annual dividends or reversionary bonuses were entitled by the relevant policies up to the respective policy year.

3.There were no actual payouts of terminal dividends/bonuses or special bonuses for the respective policy year because:

- -no terminal dividends/bonuses or special bonuses were entitled by the relevant policies up to the respective policy year; or

- -there were no terminations and/or other applicable events triggering the actual payouts of terminal dividends/bonuses or special bonuses in the reporting year for the relevant policies.

The following tables show the non-guaranteed dividends/bonuses fulfillment ratios for each product series which has new policies issued by Sun Life Hong Kong Limited (the "Company") since 2010 and still has policies inforce in the current reporting year. The fulfillment ratio is calculated as the average ratio of non-guaranteed dividends/bonuses actually declared/paid against the illustrated amounts at the point of sale. Fulfillment ratios are for reference only, dividend/bonus history is not an indicator of future declaration/performance of the participating products.

Products with the same features but with different pricing information (e.g. with different level of guaranteed and non-guaranteed benefit, premium rate, etc.) or different policy currency may be grouped into the same product series if differences in fulfillment ratios are considered immaterial. The disclosed fulfillment ratios are for basic plans only and all relevant policies are included in the calculation. In addition, to be consistent with the illustration basis, the actual amounts are calculated up to the respective policy anniversary.

Fulfillment Ratios for Reversionary Bonuses for Reporting Year 2023 of respective products

| Product | Product Type | Policy Year 1 (policies effective in 2022) | Policy Year 2 (policies effective in 2021) | Policy Year 3 (policies effective in 2020) | Policy Year 4 (policies effective in 2019) | Policy Year 5 (policies effective in 2018) | Policy Year 6 (policies effective in 2017) | Policy Year 7 (policies effective in 2016) | Policy Year 8 (policies effective in 2015) | Policy Year 9 (policies effective in 2014) | Policy Year 10 (policies effective in 2013) | Policy Year 10+ (policies effective in 2010 - 2012) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| SunGift Global | Participating Whole Life | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched |

Fulfillment Ratios for Terminal Dividends/Bonuses or Special Bonuses for Reporting Year 2023 of respective products

| Product | Product Type | Policy Year 1 (policies effective in 2022) | Policy Year 2 (policies effective in 2021) | Policy Year 3 (policies effective in 2020) | Policy Year 4 (policies effective in 2019) | Policy Year 5 (policies effective in 2018) | Policy Year 6 (policies effective in 2017) | Policy Year 7 (policies effective in 2016) | Policy Year 8 (policies effective in 2015) | Policy Year 9 (policies effective in 2014) | Policy Year 10 (policies effective in 2013) | Policy Year 10+ (policies effective in 2010 - 2012) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| SunGift Global | Participating Whole Life | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched |

Remarks:

Some of the above fulfillment ratios may show "N/A" (not applicable) due to one or more of the following reasons:

1.No relevant policies for the respective policy year because:

- -no policies were issued during a particular calendar year; and/or

- -no policies remain inforce by the end of the reporting year.

2.No annual dividends or reversionary bonuses were entitled by the relevant policies up to the respective policy year.

3.There were no actual payouts of terminal dividends/bonuses or special bonuses for the respective policy year because:

- -no terminal dividends/bonuses or special bonuses were entitled by the relevant policies up to the respective policy year; or

- -there were no terminations and/or other applicable events triggering the actual payouts of terminal dividends/bonuses or special bonuses in the reporting year for the relevant policies.

The following tables show the non-guaranteed dividends/bonuses fulfillment ratios for each product series which has new policies issued by Sun Life Hong Kong Limited (the "Company") since 2010 and still has policies inforce in the current reporting year. The fulfillment ratio is calculated as the average ratio of non-guaranteed dividends/bonuses actually declared/paid against the illustrated amounts at the point of sale. Fulfillment ratios are for reference only, dividend/bonus history is not an indicator of future declaration/performance of the participating products.

Products with the same features but with different pricing information (e.g. with different level of guaranteed and non-guaranteed benefit, premium rate, etc.) or different policy currency may be grouped into the same product series if differences in fulfillment ratios are considered immaterial. The disclosed fulfillment ratios are for basic plans only and all relevant policies are included in the calculation. In addition, to be consistent with the illustration basis, the actual amounts are calculated up to the respective policy anniversary.

Fulfillment Ratios for Reversionary Bonuses for Reporting Year 2023 of respective products

| Product | Product Type | Policy Year 1 (policies effective in 2022) | Policy Year 2 (policies effective in 2021) | Policy Year 3 (policies effective in 2020) | Policy Year 4 (policies effective in 2019) | Policy Year 5 (policies effective in 2018) | Policy Year 6 (policies effective in 2017) | Policy Year 7 (policies effective in 2016) | Policy Year 8 (policies effective in 2015) | Policy Year 9 (policies effective in 2014) | Policy Year 10 (policies effective in 2013) | Policy Year 10+ (policies effective in 2010 - 2012) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| SunJoy | Participating Whole Life | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched |

Fulfillment Ratios for Terminal Dividends/Bonuses or Special Bonuses for Reporting Year 2023 of respective products

| Product | Product Type | Policy Year 1 (policies effective in 2022) | Policy Year 2 (policies effective in 2021) | Policy Year 3 (policies effective in 2020) | Policy Year 4 (policies effective in 2019) | Policy Year 5 (policies effective in 2018) | Policy Year 6 (policies effective in 2017) | Policy Year 7 (policies effective in 2016) | Policy Year 8 (policies effective in 2015) | Policy Year 9 (policies effective in 2014) | Policy Year 10 (policies effective in 2013) | Policy Year 10+ (policies effective in 2010 - 2012) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| SunJoy | Participating Whole Life | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched |

Remarks:

Some of the above fulfillment ratios may show "N/A" (not applicable) due to one or more of the following reasons:

1.No relevant policies for the respective policy year because:

- -no policies were issued during a particular calendar year; and/or

- -no policies remain inforce by the end of the reporting year.

2.No annual dividends or reversionary bonuses were entitled by the relevant policies up to the respective policy year.

3.There were no actual payouts of terminal dividends/bonuses or special bonuses for the respective policy year because:

- -no terminal dividends/bonuses or special bonuses were entitled by the relevant policies up to the respective policy year; or

- -there were no terminations and/or other applicable events triggering the actual payouts of terminal dividends/bonuses or special bonuses in the reporting year for the relevant policies.

The following tables show the non-guaranteed dividends/bonuses fulfillment ratios for each product series which has new policies issued by Sun Life Hong Kong Limited (the "Company") since 2010 and still has policies inforce in the current reporting year. The fulfillment ratio is calculated as the average ratio of non-guaranteed dividends/bonuses actually declared/paid against the illustrated amounts at the point of sale. Fulfillment ratios are for reference only, dividend/bonus history is not an indicator of future declaration/performance of the participating products.

Products with the same features but with different pricing information (e.g. with different level of guaranteed and non-guaranteed benefit, premium rate, etc.) or different policy currency may be grouped into the same product series if differences in fulfillment ratios are considered immaterial. The disclosed fulfillment ratios are for basic plans only and all relevant policies are included in the calculation. In addition, to be consistent with the illustration basis, the actual amounts are calculated up to the respective policy anniversary.

Fulfillment Ratios for Reversionary Bonuses for Reporting Year 2023 of respective products

| Product | Product Type | Policy Year 1 (policies effective in 2022) | Policy Year 2 (policies effective in 2021) | Policy Year 3 (policies effective in 2020) | Policy Year 4 (policies effective in 2019) | Policy Year 5 (policies effective in 2018) | Policy Year 6 (policies effective in 2017) | Policy Year 7 (policies effective in 2016) | Policy Year 8 (policies effective in 2015) | Policy Year 9 (policies effective in 2014) | Policy Year 10 (policies effective in 2013) | Policy Year 10+ (policies effective in 2010 - 2012) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| SunJoy Global | Participating Whole Life | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched |

Fulfillment Ratios for Terminal Dividends/Bonuses or Special Bonuses for Reporting Year 2023 of respective products

| Product | Product Type | Policy Year 1 (policies effective in 2022) | Policy Year 2 (policies effective in 2021) | Policy Year 3 (policies effective in 2020) | Policy Year 4 (policies effective in 2019) | Policy Year 5 (policies effective in 2018) | Policy Year 6 (policies effective in 2017) | Policy Year 7 (policies effective in 2016) | Policy Year 8 (policies effective in 2015) | Policy Year 9 (policies effective in 2014) | Policy Year 10 (policies effective in 2013) | Policy Year 10+ (policies effective in 2010 - 2012) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| SunJoy Global | Participating Whole Life | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched |

Remarks:

Some of the above fulfillment ratios may show "N/A" (not applicable) due to one or more of the following reasons:

1.No relevant policies for the respective policy year because:

- -no policies were issued during a particular calendar year; and/or

- -no policies remain inforce by the end of the reporting year.

2.No annual dividends or reversionary bonuses were entitled by the relevant policies up to the respective policy year.

3.There were no actual payouts of terminal dividends/bonuses or special bonuses for the respective policy year because:

- -no terminal dividends/bonuses or special bonuses were entitled by the relevant policies up to the respective policy year; or

- -there were no terminations and/or other applicable events triggering the actual payouts of terminal dividends/bonuses or special bonuses in the reporting year for the relevant policies.

The following tables show the non-guaranteed dividends/bonuses fulfillment ratios for each product series which has new policies issued by Sun Life Hong Kong Limited (the "Company") since 2010 and still has policies inforce in the current reporting year. The fulfillment ratio is calculated as the average ratio of non-guaranteed dividends/bonuses actually declared/paid against the illustrated amounts at the point of sale. Fulfillment ratios are for reference only, dividend/bonus history is not an indicator of future declaration/performance of the participating products.

Products with the same features but with different pricing information (e.g. with different level of guaranteed and non-guaranteed benefit, premium rate, etc.) or different policy currency may be grouped into the same product series if differences in fulfillment ratios are considered immaterial. The disclosed fulfillment ratios are for basic plans only and all relevant policies are included in the calculation. In addition, to be consistent with the illustration basis, the actual amounts are calculated up to the respective policy anniversary.

Fulfillment Ratios for Reversionary Bonuses for Reporting Year 2023 of respective products

| Product | Product Type | Policy Year 1 (policies effective in 2022) | Policy Year 2 (policies effective in 2021) | Policy Year 3 (policies effective in 2020) | Policy Year 4 (policies effective in 2019) | Policy Year 5 (policies effective in 2018) | Policy Year 6 (policies effective in 2017) | Policy Year 7 (policies effective in 2016) | Policy Year 8 (policies effective in 2015) | Policy Year 9 (policies effective in 2014) | Policy Year 10 (policies effective in 2013) | Policy Year 10+ (policies effective in 2010 - 2012) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| SunWing | Participating Whole Life | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched |

Fulfillment Ratios for Terminal Dividends/Bonuses or Special Bonuses for Reporting Year 2023 of respective products

| Product | Product Type | Policy Year 1 (policies effective in 2022) | Policy Year 2 (policies effective in 2021) | Policy Year 3 (policies effective in 2020) | Policy Year 4 (policies effective in 2019) | Policy Year 5 (policies effective in 2018) | Policy Year 6 (policies effective in 2017) | Policy Year 7 (policies effective in 2016) | Policy Year 8 (policies effective in 2015) | Policy Year 9 (policies effective in 2014) | Policy Year 10 (policies effective in 2013) | Policy Year 10+ (policies effective in 2010 - 2012) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| SunWing | Participating Whole Life | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched |

Remarks:

Some of the above fulfillment ratios may show "N/A" (not applicable) due to one or more of the following reasons:

1.No relevant policies for the respective policy year because:

- -no policies were issued during a particular calendar year; and/or

- -no policies remain inforce by the end of the reporting year.

2.No annual dividends or reversionary bonuses were entitled by the relevant policies up to the respective policy year.

3.There were no actual payouts of terminal dividends/bonuses or special bonuses for the respective policy year because:

- -no terminal dividends/bonuses or special bonuses were entitled by the relevant policies up to the respective policy year; or

- -there were no terminations and/or other applicable events triggering the actual payouts of terminal dividends/bonuses or special bonuses in the reporting year for the relevant policies.

The following tables show the non-guaranteed dividends/bonuses fulfillment ratios for each product series which has new policies issued by Sun Life Hong Kong Limited (the "Company") since 2010 and still has policies inforce in the current reporting year. The fulfillment ratio is calculated as the average ratio of non-guaranteed dividends/bonuses actually declared/paid against the illustrated amounts at the point of sale. Fulfillment ratios are for reference only, dividend/bonus history is not an indicator of future declaration/performance of the participating products.

Products with the same features but with different pricing information (e.g. with different level of guaranteed and non-guaranteed benefit, premium rate, etc.) or different policy currency may be grouped into the same product series if differences in fulfillment ratios are considered immaterial. The disclosed fulfillment ratios are for basic plans only and all relevant policies are included in the calculation. In addition, to be consistent with the illustration basis, the actual amounts are calculated up to the respective policy anniversary.

Fulfillment Ratios for Reversionary Bonuses for Reporting Year 2023 of respective products

| Product | Product Type | Policy Year 1 (policies effective in 2022) | Policy Year 2 (policies effective in 2021) | Policy Year 3 (policies effective in 2020) | Policy Year 4 (policies effective in 2019) | Policy Year 5 (policies effective in 2018) | Policy Year 6 (policies effective in 2017) | Policy Year 7 (policies effective in 2016) | Policy Year 8 (policies effective in 2015) | Policy Year 9 (policies effective in 2014) | Policy Year 10 (policies effective in 2013) | Policy Year 10+ (policies effective in 2010 - 2012) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| SunGrowth | Participating Whole Life | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched |

Fulfillment Ratios for Terminal Dividends/Bonuses or Special Bonuses for Reporting Year 2023 of respective products

| Product | Product Type | Policy Year 1 (policies effective in 2022) | Policy Year 2 (policies effective in 2021) | Policy Year 3 (policies effective in 2020) | Policy Year 4 (policies effective in 2019) | Policy Year 5 (policies effective in 2018) | Policy Year 6 (policies effective in 2017) | Policy Year 7 (policies effective in 2016) | Policy Year 8 (policies effective in 2015) | Policy Year 9 (policies effective in 2014) | Policy Year 10 (policies effective in 2013) | Policy Year 10+ (policies effective in 2010 - 2012) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| SunGrowth | Participating Whole Life | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched | Not yet launched |

Remarks: